Spring in Northwest Ohio means one thing: storm season. And over the last few years, Lima and the surrounding area have been hit with more frequent high-wind events, severe thunderstorms, and the kind of weather that leaves trees on roofs and siding in the neighbor's yard.

After every major storm, we get a flood of calls with the same basic question: "Does my insurance cover this?" The honest answer is: it depends on the type of damage and how it happened. Let's break it down clearly.

What Standard Home Insurance Does Cover After a Storm

The good news first. Most standard homeowner's insurance policies in Ohio do cover wind and storm damage under what's called "open perils" or "all-risk" coverage for the structure of your home. This typically includes:

- Wind damage to your roof, siding, windows, and walls

- Damage from falling trees or branches (including your neighbor's tree that falls on your property)

- Hail damage to the roof, gutters, and exterior

- Rain damage that enters through a hole created by a covered peril — for example, rain that comes in after wind blows off a section of your roof

- Damage to detached structures like garages and sheds, typically up to 10% of your dwelling coverage

Important: If a tree falls on your house and damages it, your insurance generally covers the structural repairs — even if the tree came from your neighbor's yard.

However, if that same tree falls in your yard and just misses the house, most policies will not cover the cost of removing it. Tree removal without structural damage is typically not covered.

What Home Insurance Does NOT Cover After a Storm

This is where a lot of Ohio homeowners get caught off guard. There are several very common types of storm-related damage that standard home insurance simply does not cover:

Flooding from storm runoff. This is one of the most common misconceptions in all of home insurance. If heavy rain causes water to flow across the ground and into your basement or home, that is flood damage — and it is not covered by your standard homeowner's policy. Flood insurance is a completely separate policy.

Sewer or drain backup. When a severe storm overwhelms the sewer system and water backs up through your drains or toilets, that's also typically not covered unless you have a specific water backup endorsement on your policy.

Gradual damage or poor maintenance. If your roof was already aging and a moderate windstorm causes shingles to lift, your carrier may argue the damage was due to wear and tear rather than the storm itself. Keeping up with maintenance matters for your claim outcome.

Your car. Vehicle damage from storms — hail dents, fallen tree branches, flooding — is not covered by home insurance. That falls under your auto insurance comprehensive coverage.

Power surges. Storm-related power surges that damage electronics or appliances are usually not covered under a standard policy. You'd need a specific equipment breakdown endorsement.

The Wind and Hail Deductible Trap

We've talked about this in depth in a recent post, but it bears repeating here because it catches so many NW Ohio homeowners off guard after a storm.

Many home insurance policies now have a separate, higher deductible that applies specifically to wind and hail claims. So even if your standard deductible is $1,500, your wind and hail deductible might be 1% or 2% of your home's insured value — which could be $3,000, $5,000, or more.

Before you file a wind or hail claim, check your declarations page for a separate wind or hail deductible line. Knowing that number before you call the claims department will help you make a more informed decision.

What to Do Immediately After Storm Damage

If your home sustains damage in a storm, the steps you take in the first few hours matter a lot for your claim outcome:

- Document everything before touching anything. Walk around the home and take photos and video of all visible damage — roof, siding, windows, gutters, interior water intrusion, everything.

- Prevent further damage. You're required under most policies to take reasonable steps to prevent additional damage. Cover a damaged area of the roof with a tarp, board up broken windows, and move belongings away from water intrusion areas. Keep receipts for any emergency repairs you make.

- Call your agent before the carrier's 1-800 line. We can walk you through whether to file, what to expect, and how to present the damage clearly to the adjuster.

- Don't let a storm chaser pressure you. After major storms in NW Ohio, roofing contractors often knock on doors offering to file insurance claims on your behalf. Be cautious — some are legitimate, many are not, and signing over your claim rights can complicate the process significantly.

Is Your Coverage Actually Ready for Storm Season?

If you haven't looked at your home insurance policy recently, spring storm season is the perfect reason to do it now. Specifically, you want to know:

- Whether you have a separate wind or hail deductible and what it is

- Whether you have flood coverage or a water backup endorsement (most people don't, and don't realize it until they need it)

- Whether your home is insured to its current replacement cost — not its market value, but what it would actually cost to rebuild it today

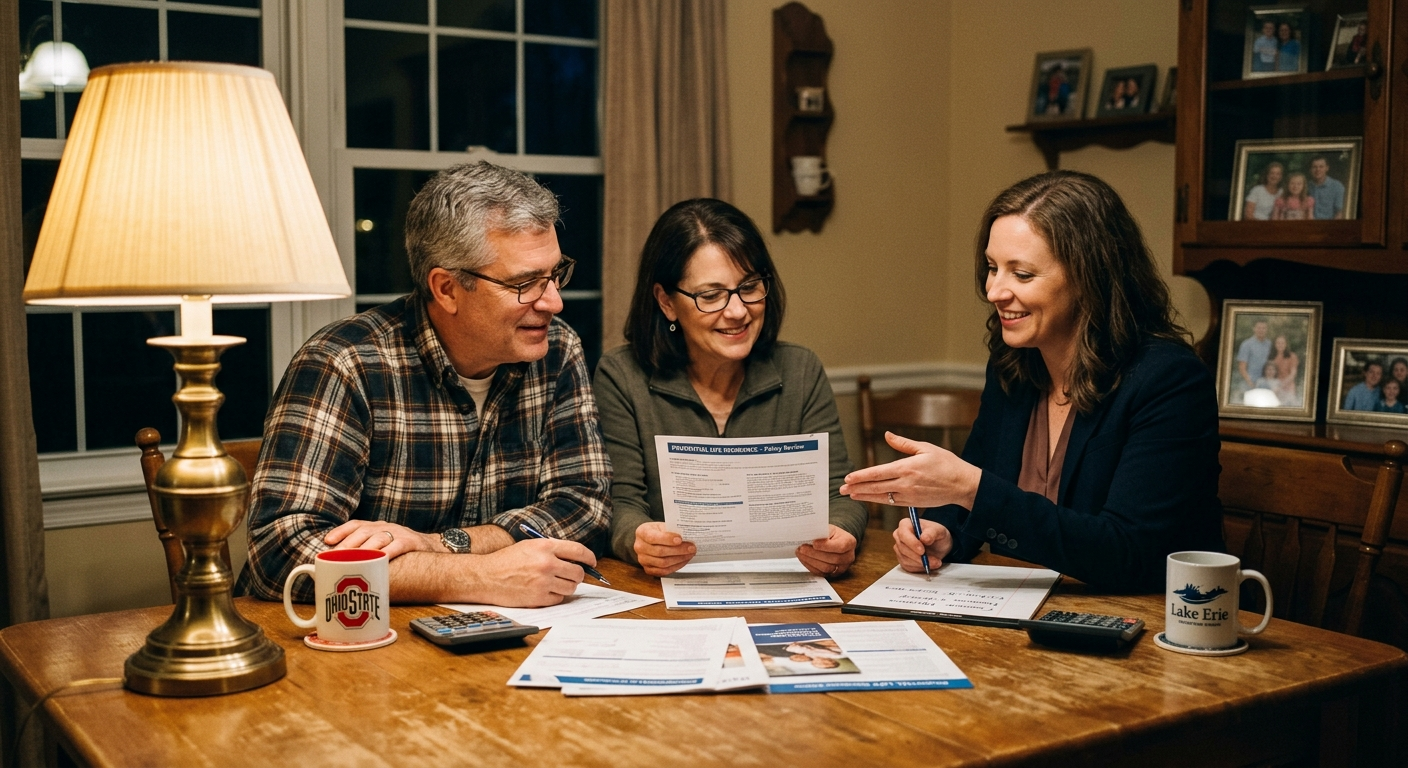

These are questions we answer every day for Lima and Northwest Ohio homeowners. If you're not sure what your policy actually covers, a 15-minute conversation with us can give you a lot of clarity — and peace of mind heading into storm season.

Call (419) 222-2454 or visit leyinsurance.com to schedule a free policy review before storm season hits full swing.

Get A Quote

At Ley Insurance Agency, securing your future is easy. Ready to protect what matters? Contact us for a quick quote and personalized insurance options!

Kelly

Speak to Kelly 24/7

Microphone ready

Start your custom insurance quote

Instant answers to your insurance questions

Schedule appointments or follow-ups

Personal Insurance

From auto and homeowners to renters and umbrella policies, we help protect your family and property. Let’s find coverage that fits your life.

Commercial Insurance

We customize policies for your industry's risks, like general liability and workers' comp, ensuring you can run your business worry-free.

Contact Ley Insurance Agency

Recent Posts